Market Reports

The Future of Disruptive Technology in Paper and Board to 2030

The world has been in the midst of the COVID-19 pandemic, which has changed the way we live. Online sales of packaged goods have increased. In North America alone, packaging demand increased by 8% during the month of April 2020. In contrast, several newspapers have gone out of business or have suffered financial hardship because of lack of advertising as society shut down. After the pandemic subsides, long term, demand for packaging will probably exceed historical averages by one or two percent, whereas newsprint will decline at a significantly greater rate than in the past.

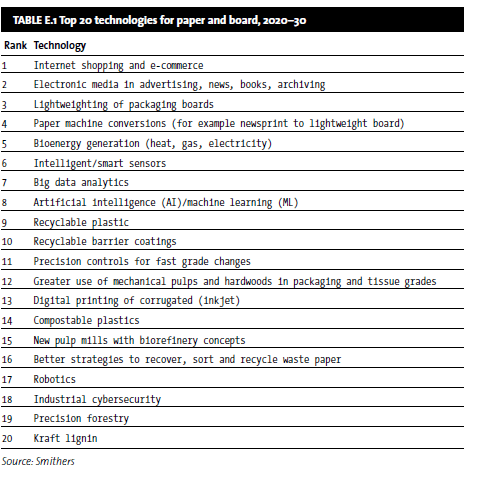

The top 20 disruptive technologies in paper and board covered in this new report from Smithers can be grouped into four general categories: Impact of the internet on consumer behaviour; digitisation of the paper and board industry; paper and board substitution for plastic; and internal transformation of the paper and board industry. The technologies with the highest likelihood of technical success have all been installed on a commercial scale to some extent, including internet shopping, electronic media, paper machine conversions, digital inkjet printing of corrugated, bioenergy generation, and lightweighting.

The internet, which has spawned e-commerce and electronic media, has had a major impact not only on the paper and board industry but on the way we work and live. Via the internet, we can now read the news and get information immediately, often for free. In the past, we sought merchandise or services by perusing classified ads in newspapers or advertisements in magazines. Now it is possible from the comfort of a computer keyboard or smartphone to search the entire world for something through platforms such as Amazon, Alibaba and eBay.

With the disappearance of advertising dollars, many newspapers in Europe and North America have folded, reduced print runs, or have moved to digital platforms. Magazines have also declined but may find a niche in luxury goods. In the US, the internet has surpassed television for advertising dollars, and e-books are now more popular than printed books.

Most technologies ranked in the top 20 are in the digitisation category. Pulp mills and paper and board machines are already highly instrumented and many functions are under computer control. Applications in the forest resource and harvesting, because of their complexities, are less advanced but are starting to enter the digital age. Key digital technologies include: Intelligent/smart sensors, Big Data analytics, artificial intelligence (AI)/machine learning (ML); precision controls for fast grade changes; digital printing of corrugated (inkjet); robotics; cybersecurity; and precision forestry. An instrumented mill is awash in data and information, some of which is used in control loops and some is displayed for operators to monitor and to help guide their decisions.

In the next decade, legislation will be in place in the US, Europe and China to ban single-use plastics and insist that most other plastic be recycled. Despite the fact that over half the paper and board in the US is recycled, less than 10% of plastics now are. Restrictions on plastics create a major opportunity for fibre-based products to fill the gap.

In response to these changes, the plastics industry is making major investments in technologies to recycle plastics, including the European Union’s “Horizon 2020” project. Compostable plastic is based on plant-based polymers such as polylactic acid (PLA) which is a sustainable raw material. If successful, these efforts will diminish paper’s advantages in recycling and thereby limit paper and board’s potential market share.

Most liquid containers, even if they are primarily composed of fibre, have polymer or foil barrier layers that cause difficulties and contamination when recycling. Recyclable barrier coatings will open up market share. Sort-at-source, digitising the collection and using robots with AI in the collection centres have also shown that improvements are possible.

For a full understanding of the impact of these and other disruptive technologies, download the brochure here.

Find out how you can attend this event for free with Smithers paper membership.

Find out how you can attend this event for free with Smithers paper membership.