Market Report

The Future of Print Equipment Markets to 2023

At the same time the market will see a transformation, with real demand growth confined to inkjet sales and certain formats of sheetfed offset litho. This is happening in response to profound and ongoing change in demand for print, and equipment manufacturers are compelled innovate to secure sales in an increasingly competitive market.

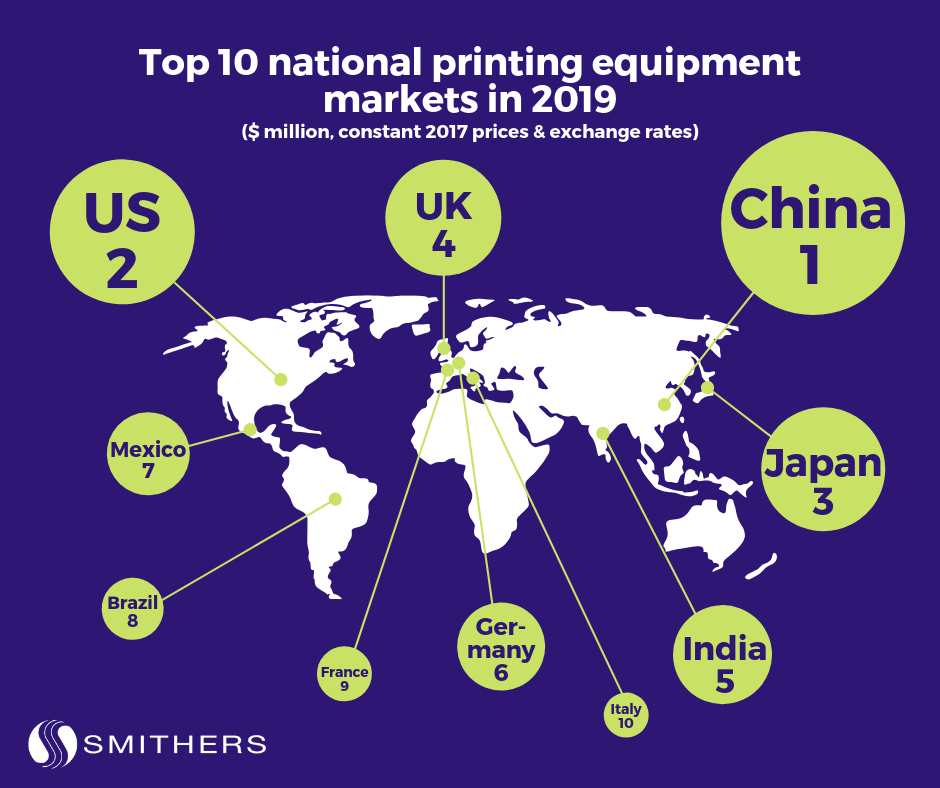

These trends and their impact on future demand for over 25 types of commercial printer are tracked and quantified in the recent Smithers report – The Future of Print Equipment Markets to 2023.

The printing industry is undergoing a series of major changes. Sales of newspapers and magazines, a traditional and important segment for print equipment, have fallen dramatically in many parts of the world in face of 24-hour digital access to news and information via computers, tablets and smartphones.

Rising demand for packaged goods means that packaging and label printing are two of the few growth sectors in print demand. Original equipment manufacturers (OEMs) are looking to capitalise this with new dedicated press formats – especially in inkjet – and extending capabilities on existing platforms to handle packaging substrates. Within packaging, and other end-use applications, print buyers are demanding shorter average print runs, and ever quicker delivery times.

OEMs of both analogue and digital print equipment are reacting to the changing market dynamics with improvements to their presses. For analogue processes, this has largely been to make them more agile and efficient to deal with a larger number of print jobs of shorter runs per day. For digital, developments have been focused on improving print quality to match analogue processes, and on increasing print line speeds.

Faced with reductions in average print run of up to 50% in some cases, analogue printers are demanding intensive technological developments. High levels of automation at all stages of the print process have allowed print service providers (PSPs) to make major reductions in make-ready times and give them greater control and monitoring of the print run to improve quality standards. Cumulatively these improvements have enhanced the flexibility of the print equipment to make PSPs to run a larger number of shorter print runs during a working shift cost-effectively.

The widespread use of computer-to-plate (CTP) processes has been a key factor in reducing prepress times. The process has been used for offset litho for more than five years, and it is rapidly gaining ground in flexo prepress. CTP also provides improved reproduction quality so that PSPs can offer better service to customers. The incorporation of digital workflow systems and the use of on-line spectrophotometers and pattern recognitions systems to constantly monitor quality during the print run have improved the efficiency of print lines and reduced running costs, as well as reducing reject rates and generation of waste.

The analogue process that has seen the biggest number of improvements in recent years is sheetfed offset litho. Innovations by the leading Western and Japanese manufacturers have transformed the technology, to a great extent.

Besides the improvements detailed above, print line run speeds have been increased and processes been optimised for short print runs. Computer-integrated manufacture systems are being used to preset the presses with files from prepress, and with simultaneous plate changing and washing cycles make-ready times can be reduced to under 10 minutes – less than three minutes for the same substrate and format. Sheedfed offset litho printers are increasingly carrying out simultaneous printing of groups of jobs by setting them up side-by-side across a large-format press.

Offset litho is also seeing a boost from orders received via the online web-to-print sector. The segment is also benefitting from a new demand for higher productivity very-large format (VLF) litho presses. As new installations of B1-B3 presses decline, Smithers’s analysis tracks how annual sales of VLF machines will more than double across 2017-2023.

In flexography, an important additional development has been in the use of sleeves to simplify the process of mounting the printing plates onto the flexo press, reducing make-ready times. This has eliminated the need for printers to prepare and store the multiple, non-interchangeable cylinders required for several jobs, reducing the costs for cylinders and for their storage.

The segment is also innovating through cooperation with inkjet press and printhead developers. This is seeing a new generation of hybrid presses that combine flexo’s efficiency for big solid area colours with the variable data potential of inkjet, integrated with existing flexo finishing lines.

Manufacturers of gravure presses have introduced automated trolley changeover processes for cylinders and inking systems on the latest generation of equipment, making them more flexible and enabling quicker turnaround times between jobs.

Technology developments of the two digital print techniques, electrophotography (toner) and inkjet, have been taking place for many years. Naturally suited to short-run commissions, these are enabling these processes to be used for a wider range of commercial and industrial printing applications. The main focus in digital printing in 2019 is on:

Electrophotography will continue to see improvements in colour printing quality to match, or exceed, that achievable by offset printing. The potential for increasing the speed of toner machines is limited however by the multi-stage print technique. This will see sales of new electrophotography equipment fall across the Smithers forecast period as genuine growth concentrates on inkjet. In response many toner OEMs are looking to diversify into this alternative digital process.

Across the print industry R&D spending is highest in inkjet. This investment is being witnesses in improvements in quality and reliability of the equipment, reducing printers’ total costs. New inkjet presses can print at faster speeds to give better productivity, and new workflow solutions and more automation of material handling is improving productivity of lower speed presses.

New sales of inkjet press are being driven by the introduction of high-performance inkjet machines, in packaging with machines directly targeted at corrugated, folding cartons, flexible and rigid plastics, and even metal print. As well as labels, there is a developing application in cost-effective production of short to medium runs of mono and full-colour books, often via e-commerce ordering.

A major trend is for digital print lines to integrate with postpress finishing systems, to take full advantage of the automated operation of the print process. This is more prevalent with inkjet lines as integrated finishing limits flexibility of a toner line. As the number of digital print lines grows at the expense of analogue printing, the use of in-line finishing for those end-use applications with good workflow streams will reduce the number of near/off-line postpress operations in print shops.

The Future of Print Equipment Markets to 2023 offers further insight and market research of trends affecting the market.